Lesson: Saving money in cash feels safe, but inflation quietly destroys its buying power. Investing is not a hobby. For long-term money, it becomes a necessity and this is another reason why we need to learn it.

I used to think saving money meant I was being responsible. But then I realized something uncomfortable: money sitting in cash is not standing still, it is shrinking in purchasing power and this was one of the many triggers which lead me to learn investing your money is the best approach.

If inflation is 3% and my bank pays 1%, I am not “earning interest” I am losing my money slowly.

This article is about why cash feels safe, why that feeling can be dangerous, and why investing long-term money is not optional if I want to protect my future purchasing power.

The mistake or question

For a long time, I thought the responsible thing was simple: work, save money, rinse and repeat, keep it in the bank, avoid risk.

That sounds mature, right? It also sounds safe, but you see, there is a problem: cash is safe only in nominal terms.

If I put $10,000 in the bank, next year I may still see $10,000 on the screen, maybe a little more if I get interest. But the real question is not: “Do I still have $10,000?”, the real question is: “What can that $10,000 still buy?”.

That is where inflation hurts. Inflation does not steal money from the bank account directly it steals purchasing power, the number stays visible BUT the value disappears quietly.

That is why inflation is dangerous for beginners, especially those who lack financial education, like me. It does not feel like a crash, there is no red candle, no alert, no scary chart. Just groceries getting more expensive. Rent going higher. Services costing more. A coffee that used to be $2 becoming $4 and all in a matter of 3 years (current reality).

And if my money is sitting still while prices are moving up, I am falling behind.

Brutal truth: Keeping all my money in cash is not avoiding risk. It is choosing a different kind of risk, the risk of guaranteed slow loss.

The simple explanation

Inflation means prices rise over time. If inflation is 3% per year, something that costs $100 today may cost around $103 next year. That does not sound dramatic. But over many years, it becomes brutal.

The formula is simple:

$$FV = PV(1 + r)^n$$

Where:

- \(PV\) = today’s value

- \(r\) = annual inflation rate

- \(n\) = number of years

- \(FV\) = future price of the same lifestyle or basket of goods

So if inflation is 3% per year:

$$ \begin{aligned} FV_{10} &= 10{,}000(1 + 0.03)^{10} \approx 13{,}439 \\ FV_{20} &= 10{,}000(1 + 0.03)^{20} \approx 18{,}061 \\ FV_{30} &= 10{,}000(1 + 0.03)^{30} \approx 24{,}273 \end{aligned} $$

| Today’s cost | After 10 years | After 20 years | After 30 years |

|---|---|---|---|

| $10,000 | $13,439 | $18,061 | $24,273 |

That means a lifestyle that costs $10,000 today could require about $24,273 in 30 years if inflation averages 3%, same lifestyle much higher price.

This is why “I will just save cash” is weak thinking for long-term money, and here it goes one good/fresh example on this matter -> Social Security COLA for 2027 projected to jump, thanks to surging inflation.

Cash protects you from short-term emergencies but cash does not protect your long-term purchasing power.

The U.S. Bureau of Labor Statistics has an inflation calculator based on CPI data, and there are similar calculators for other countries. The exact country matters, but the principle is universal: when prices rise, cash buys less and you can check yourself -> CPI Inflation Calculator.

The personal reality check

Last week I was bored, so I opened a Romanian inflation calculator and typed in 100 lei from 2010. The site told me that 100 lei back then is worth about 9 USD today. My country of origin is Romania, if that was not already obvious, and the result was uncomfortable.

The calculator showed how much purchasing power changed between 2010 and 2026. I stared at the number for maybe a minute because it made the idea, real -> Inflation Calculator.

This was not some abstract investing theory, this was my own country, my own currency, my own lifetime and here is the part that bothered me: if you’d asked 2010-me what the responsible thing to do with 100 lei was, I would have said “put it in the bank”. And I would have meant it! That was the adult answer, the mature answer, the non-greedy answer but 2026-me now understands that the adult answer was incomplete.

Saving money was good, but saving money without understanding inflation was not enough.

A real example: $10,000 over 30 years

Now let’s run a thought exercise, let’s imagine we have $10,000.

I have three choices: 1. Keep it under the pillow. 2. Put it in a savings deposit. 3. Invest it in a broad stock market index fund (because we’re starting from zero we’ll cover stock-picking in a later post, for now ETF is perfect).

This is not investment advice. This is a thinking exercise.

Assumptions:

| Option | Annual return | Inflation | Real result |

|---|---|---|---|

| Cash under pillow | 0% | 3% | Losing purchasing power |

| Savings deposit | 1.5% | 3% | Still losing, but slower |

| Broad index fund | 7% | 3% | Growing purchasing power |

The FDIC reported a national savings rate of 0.38% and 12-month CD rate of 1.62% in June 2025, while FRED also tracks national savings deposit rates from FDIC data. Rates change, but the important point is that normal savings rates can easily sit below inflation.

Just to understand how I got those average number of 7% ( the number is not magic) please do consult these links, there are many more but if you want to do your own checks, this would be a good way to start :

- Historical Average Stock Market Returns for S&P 500 (5-year to 150-year averages)

- S&P 500 Historical Annual Returns (1927-2026)

- Average Stock Market Return Last 30 Years

- 31 Years of Stock Market Returns

- What Is the Average Stock Market Return?

- What Is the Average Stock Market Return?

And this is important: “Average return” is a dangerous phrase. Your actual return will not match the market average if you are concentrated in individual stocks, expensive sectors, hype companies, or bad businesses.

Your result depends on what you own, what price you paid, how long you hold, if you used leverage (fees need to be paid), broker commissions will be subtracted and yes, whether you panic at the wrong time.

But for the sake of understanding inflation and compounding, we can use 7% as a simple long-term example which also has some evidence based on above links.

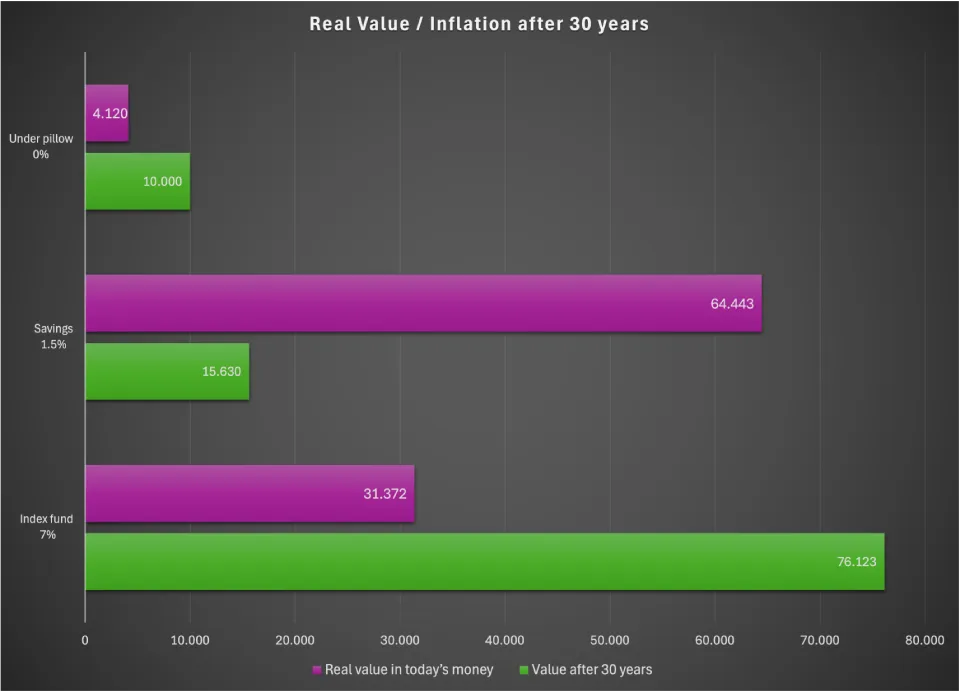

Now let’s see the numbers, nominal value after 30 years:

| Option | Starting amount | Annual return | Value after 30 years |

|---|---|---|---|

| Under pillow | $10,000 | 0% | $10,000 |

| Savings deposit | $10,000 | 1.5% | $15,630 |

| Index fund | $10,000 | 7% | $76,123 |

At first, the savings deposit looks okay $10,000 becomes $15,630, but that is the trap, we also need to adjust for inflation.

Real purchasing power after 30 years if inflation is 3%, then future money is worth less:

| Option | Nominal value | Real value in today’s money |

|---|---|---|

| Under pillow | $10,000 | $4,120 |

| Savings deposit | $15,630 | $6,443 |

| Index fund | $76,123 | $31,372 |

And well, we just got to the reality, this is the part that hurts.

Under the pillow, I still have $10,000 after 30 years. But in today’s purchasing power, it is only worth about $4,120, that is not safety, that is slow destruction.

This graph shows what the account balance may look like, nominal numbers can lie adding on top inflation-adjusted gives us a pretty neat picture. This is the graph beginners need to see, the bank balance may go up and the real value can still go down.

That is the difference between nominal money and real money.

Why beginners get it wrong

Beginners get this wrong because cash feels safe and investing feels risky, or at least discussing with people around, this is always what I get in return as an answer and emotionally, that makes sense.

Cash does not move up and down every day, it sits in your wallet, you can see it.

A savings account does not show a 20% drawdown, the stock market can, but this creates a dangerous illusion.

Trap 1: Confusing stability with safety

Cash is stable in number but it is unstable in purchasing power. If prices double over time and my cash does not double, I become poorer even if the bank balance looks unchanged and that is the silent trick.

The account balance says:

You still have your money.

Inflation says:

No, you do not.

There are two numbers you need to learn to separate and most of us, especially those who lack financial education, only watch one. Nominal return is what the bank shows you. “Your savings account earns 3% per year”.

Real return is what you can actually buy with that money after inflation and yes, we have a formula for it too: $$\text{Real return} \approx \text{Nominal return} - \text{Inflation}$$

If your bank gives you 3% and inflation is 7%, your real return is −4%. You have more money on the screen, and “less butter in your fridge”.

That negative number is the real result, the brokerage app doesn’t show it, neither does the banking app. Both will happily display a positive interest rate, while you lose purchasing power every month.

Here’s the brutal reframe: inflation is a tax on people who don’t invest. It’s not announced, not voted on, not avoidable by being careful, its just a bad mechanism created by our “greatest” financial system. It just shows up on food, rent, electricity, every purchase. And inflation never refunds..

Trap 2: Thinking saving and investing are enemies

Saving and investing are not enemies, they solve different problems.

Cash is for:

- emergency fund

- rent

- food

- short-term needs

- money needed soon

- psychological safety

Investing is for:

- long-term wealth

- retirement

- beating inflation

- owning productive assets

- growing purchasing power

- why not, financial independence

The beginner mistake (or almost all humans without a financial education) use cash for everything. That feels responsible, but it is incomplete.

Trap 3: Waiting for the “perfect time”

A beginner often says: “I will invest later, when I understand more.”

That sounds reasonable, but “later” can become five years or more and during those five years, inflation keeps working, inflation does not sleep.

The market will not wait until I feel confident, inflation will not pause because I am nervous. This does not mean I should throw all my money into stocks tomorrow. That would be stupid. It means I/we need a process, a simple process beats endless hesitation. We need to craft a strategy of flexibility and opportunism.

Trap 4: Ignoring real return

The only return that really matters is real return. Real return means, investment return minus inflation.

Example:

| Investment return | Inflation | Real return |

|---|---|---|

| 1.5% | 3% | -1.5% |

| 5% | 3% | 2% |

| 8% | 3% | 5% |

If my savings deposit pays 1.5% while inflation is 3%, I am not truly gaining, I am losing purchasing power, I am just losing it politely.

The investing comparison

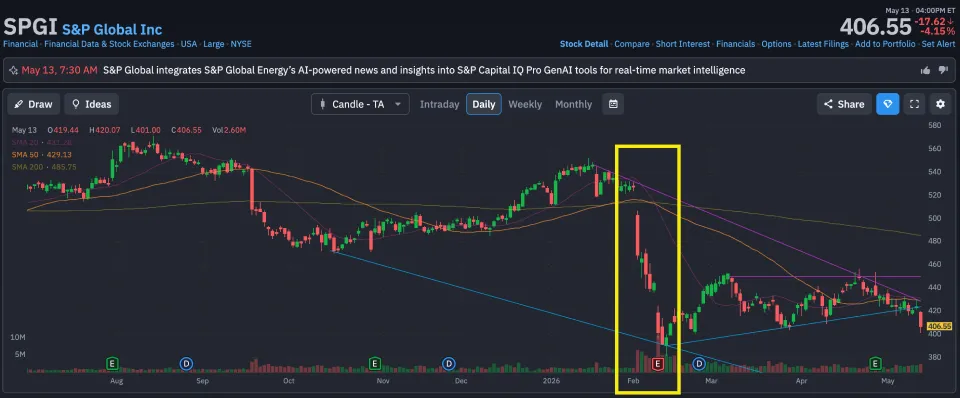

This is where people get emotional and someone will say: “But stocks can crash!”, which is correct, yes, stocks can crash. A broad index fund can fall 20%, 30%, even 50% during severe bear markets or during very bad news like for example Iran war, Strait of Hormuz closed just see below what was the impact in a couple of days against S&P500 (what is this you may ask, we will touch it in another blog article).

That is real risk, but long-term investing is not about pretending crashes do not happen, it is more, in my view, about asking a better question: “Which risk am I willing to take?”

Cash has inflation risk, stocks have volatility risk and the difference is this inflation risk is quiet and almost guaranteed over long periods, while stock volatility is loud, scary and uncomfortable, but historically, patient investors in broad productive assets have been rewarded for taking that risk (trading is different we’ll cover that in a future post).

The S&P 500 has had many bad years, including 2008, when total return was about -37%, and 2022, when total return was about -18.11% (info in my above links). But over long periods, broad equity ownership has historically produced positive nominal returns because investors own productive companies, not just paper.

This is why I should not think: “Cash is safe. Stocks are risky.”

A better version would be: “Cash is safer short term. Productive assets are usually better long term.” and that one sentence changes the whole decision.

My current rule

My current rule is: Cash is for short-term safety. Investing is for long-term purchasing power.

I should not keep all my money in cash just because I am afraid of investing, but I also should not invest money I may need soon and this is how I got to my simple framework:

| Time horizon | Better place for money |

|---|---|

| 0–6 months | Cash / current account |

| 6–12 months | Emergency fund / savings deposit |

| 1–5 years | Investing money depends on the goal, risk tolerance, and flexibility |

| 5+ years | Consider diversified investing |

| 10+ years | Investing becomes harder to ignore |

This is not perfect. But it is much better than “everything in cash because I am scared.” or for any possible reason which you can find! Brutal truth: If I keep long-term money in cash forever, I am not being conservative. I am refusing to learn — and we are living in times where if you don’t learn, you become obsolete on day two.

Simple checklist: Am I holding too much cash?

Ask these questions:

- Do I have an emergency fund?

- How many months of expenses does it cover?

- Do I need this money in the next 6 months?

- Is my savings rate below inflation?

- Am I holding cash because I have a plan or because I am afraid?

- Do I understand the difference between nominal return and real return?

- Do I have a monthly investing plan?

- Am I diversified, or am I gambling on one stock?

- Would I panic if my investment dropped 20%?

- Have I written down my investing rules?

If I cannot answer these, I do not have a strategy, I have a pile of money and emotions and yes, having a pile of money is better than having no money -> Warren Buffett - “An idiot with a plan can beat a genius without a plan.”.

That does not mean invest everything, it means stop pretending cash has no risk.

Your first investing decision is not which stock to buy, your first investing decision is:

“Which money must stay safe, and which money must start having a job?”

Some money must protect me from short-term chaos, some money must fight long-term inflation that is the real decision which you have to make.

Final thought

Saving money is good, saving money is necessary but saving alone is not enough.

That was my mistake, I thought the enemy was losing money in the market, when the real enemy is losing purchasing power while doing nothing.

Inflation is not dramatic, it does not look like a crash. It looks like normal life becoming more expensive every year, so the goal is not to become reckless, the goal is to become realistic.

Cash protects me from short-term chaos, investing protects me from long-term decay and I need both and if I keep all my long-term money under the pillow or in low-interest deposits forever, I should be honest about what I am doing:

- I am not avoiding risk.

- I am accepting inflation as my guaranteed opponent.

Time to change that!

Comments

0